This guide explains how to file a 2000 direct deposit claim, what documents you need, and the deadlines you must meet. It is written in practical, step-by-step language so you can act quickly and confidently.

Who should file a 2000 direct deposit claim

If a scheduled direct deposit of 2000 did not arrive in your account, you may be eligible to file a claim. Typical situations include bank errors, employer payroll mistakes, or electronic transfer failures.

Before filing, confirm the expected payment details with the payer and check your bank records for pending or returned deposits.

Key deadlines for a 2000 direct deposit claim

Deadlines vary by payer and institution, but acting promptly improves the chance of recovery. Common timelines include:

- Contacting your bank: within 24–72 hours of the missed deposit.

- Filing a formal claim with the payer or payroll provider: within 30 days when possible.

- Bank error disputes under electronic funds rules: typically within 60 days of your statement date.

Missing a deadline can limit remedies, so start the process immediately after you notice the problem.

Steps to file a 2000 direct deposit claim

Follow these clear steps to file a claim and track resolution. Keep records at every stage.

1. Confirm the missing deposit

Check your bank account activity for pending transactions or reversals. Look at pay stubs, employer payroll notices, or payment confirmation emails.

Note the date the payment was supposed to arrive and any reference or confirmation numbers.

2. Contact the payer

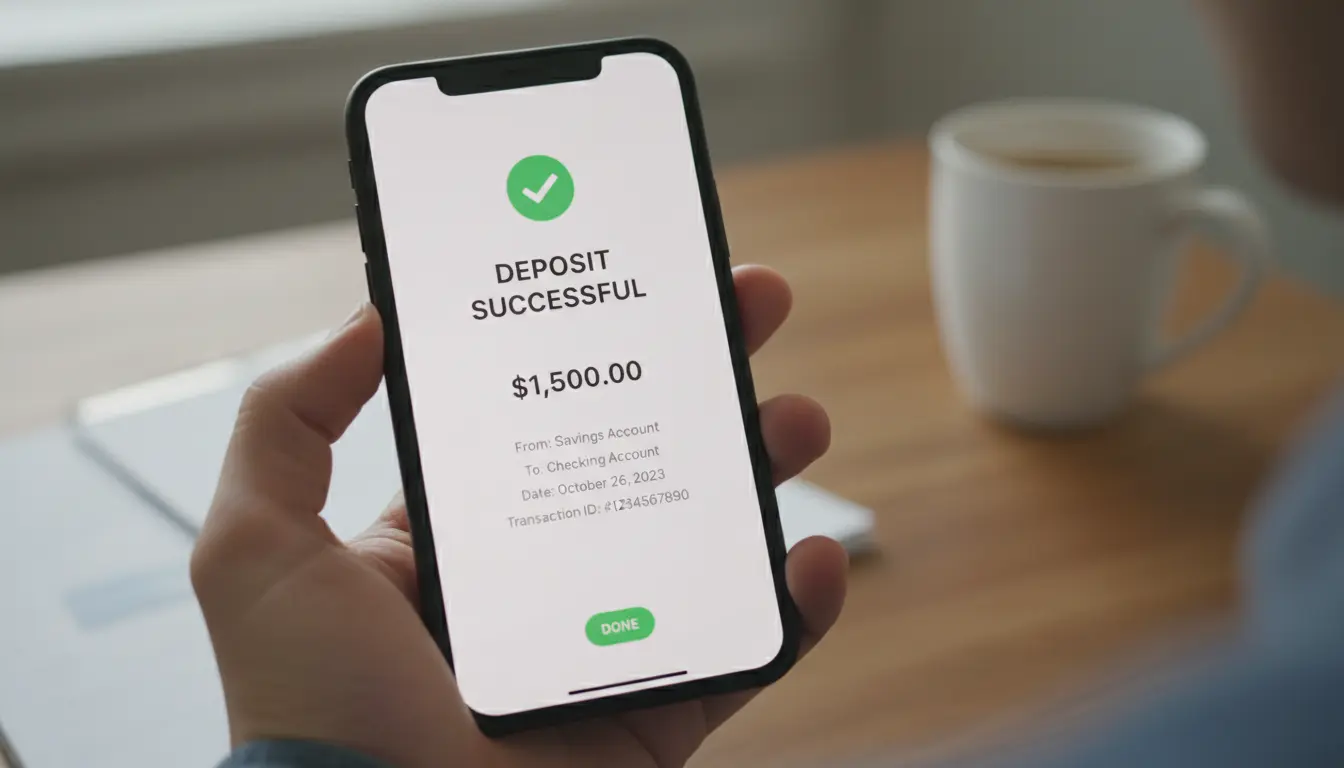

Notify the employer, government agency, or payer immediately. Provide the payment date, amount (2000), and any reference numbers.

Ask them to confirm whether the transfer was sent and the routing/account information used.

3. Contact your bank

Call or visit your bank to report the missing deposit. Provide transaction dates, amounts, and any confirmation numbers from the payer.

Request a trace or investigation under your bank’s electronic transfer dispute process.

4. Gather required documents

Most claim processes require clear documentation. Prepare digital copies or photocopies of:

- Pay stubs, payroll reports, or deposit notifications showing the 2000 amount.

- Bank account statements showing no receipt of the 2000 deposit.

- Correspondence with the payer or bank (emails, messages).

- Identification (government ID) if required by your bank.

5. File the formal claim

Submit the claim through the payer’s payroll portal, the bank’s dispute form, or by certified mail when required. Use the method the payer or bank specifies for fastest handling.

Keep a copy of each submission and note any claim or reference numbers the provider gives you.

6. Track the claim and follow up

Set reminders to follow up if you do not receive updates within the timeframe given. Most institutions provide a case or ticket number.

If the claim stalls, escalate to a supervisor or the payer’s compliance or payroll department.

What to expect after filing a 2000 direct deposit claim

Investigations often take several business days to a few weeks, depending on complexity. Banks may perform an electronic funds trace to locate the transfer.

Possible outcomes include the payment posting to your account, a corrected resubmission by the payer, or determination that funds were misdirected and require retrieval.

Common issues and how to avoid them

- Wrong account or routing number: Confirm account details with the payer beforehand.

- Timing differences: Some transfers can take 1–3 business days; check cutoff times and weekends.

- Unclear names or memos: Ask payers to include your account number or identifier in the transfer memo.

Practical tips for faster resolution

- Document every contact and retain screenshots of online portals.

- Request written confirmation of actions from your payer and bank.

- Use certified mail when sending signed dispute forms to create a verifiable trail.

- Keep copies of your ID and account statements ready to submit quickly.

Under common banking rules, you typically have 60 days from the statement date to dispute an unauthorized electronic transfer. Acting sooner often yields faster recovery for missed direct deposits.

Case study: Quick action recovered a 2000 deposit

Maria, a retail manager, noticed a 2000 payroll deposit missing on Friday morning. She emailed payroll immediately and called her bank the same day. Payroll confirmed a routing typo and resubmitted the transfer on Monday.

The bank completed the trace and posted the corrected deposit within four business days. Maria kept copies of all communications and the payroll confirmation, which sped up the investigation.

When to escalate or get help

If your bank or payer does not resolve the claim within a reasonable time, consider these options:

- Ask to speak with a supervisor or the payer’s payroll compliance team.

- File a complaint with your national banking regulator or consumer protection agency.

- Seek legal advice if the amount is large or the payer refuses to cooperate.

Final checklist before you file

- Confirm the missing amount and expected date (2000 and date).

- Collect pay stubs, bank statements, and correspondence.

- Contact the payer and bank immediately and log each contact.

- Submit the formal claim with documentation and keep reference numbers.

Filing a 2000 direct deposit claim is straightforward when you act quickly and document everything. Use the steps above to organize your claim and increase the chance of a timely recovery.